By Joz Coetzer

![]()

While credit ratings are designed to assess the creditworthiness of country or corporation to inform the decisions of investors in these entities, the considerations of credit rating agencies may not always be fully aligned with those of investors. However, given a government’s responsibility for delivering infrastructure and power and, as a result, its key role throughout the term of a project, it is not a stretch of the imagination that sovereign credit ratings may be noteworthy to investors in projects, particularly in emerging markets.

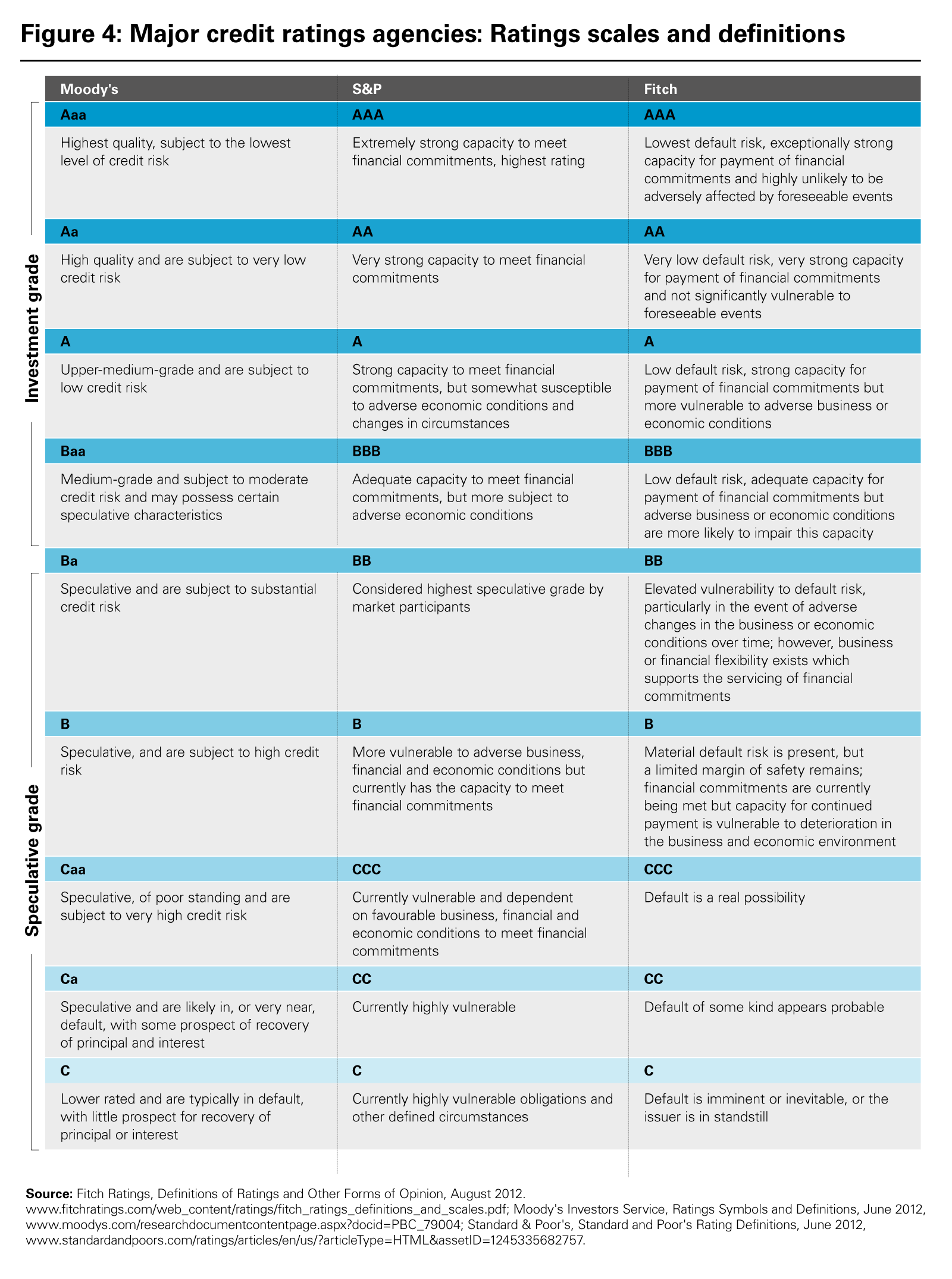

The leading credit rating agencies, Fitch, Moody’s and Standard & Poor’s, use variations of a sliding scale of letter-based grades to rank debtors from ‘AAA’ to ‘C’. ‘A’- rated entities are sub-categorised as prime, high-grade or upper medium-grade entities and are associated with relatively low risk of default. ‘BBB’ ratings (or ‘Baa’ ratings by Moody’s) are given to lower medium-grade entities, and ratings of ‘BB’ or ‘Ba’ are ranked as noninvestment-grade.

Earlier this year, Fitch and Standard & Poor’s downgraded the South African government’s long-term foreign currency rating to sub-investment-grade at ‘BB+’, from the previous lower medium-grade rating of ‘BBB-‘. While Moody’s did not follow suit to rank South Africa at speculative status, it downgraded the long-term issuer and senior unsecured ratings of South Africa by two notches within the space of two months from Baa1 to Baa3, just one notch above sub-investment-grade. The decisions of the leading credit rating agencies to downgrade the debt ratings of South Africa necessitate a consideration of implications of the downgrades that would be notable to investors in the project finance industry.

In this article:

- We consider the implications of the recent downgrades of the South African government by the leading credit rating agencies to project finance

- We offer insight into options that may enhance project credit risk and secure the confidence of investors considering financing projects in South Africa

Contents:

- Relevance of sovereign credit ratings and implications of South Africa’s downgrades for project finance

- Credit ratings comparisons on the continent

- Options for enhancing project credit risk

- Prospects for South Africa

Relevance of sovereign credit ratings and implications of South Africa’s downgrades for project finance

Credit ratings are a measure of the economic strength of the sovereign and seek to measure the likelihood of debts being repaid on time. Rating agencies assess select key macroeconomic and socioeconomic indicators to determine a debtor’s ability and willingness to honour financial obligations.

Rating criteria for governments focus on institutional, economic and fiscal strength by assessing the following indicators:

- Economic structure and performance, including real GDP, per capita income, headline inflation rate, gross investment as a percentage of GDP and gross domestic savings as a percentage of GDP

- Government finances, including government revenue to GDP, government expenditure to GDP, government debt to GDP, debt interest payment to revenue and the budget balance as a percentage of GDP

- External payments and debt, including current account balance as a percentage of GDP, the ratio of external debt to GDP and level of official reserves

- Susceptibility to political risk, socioeconomic risk and external vulnerability risk as well as institutional independence

The leading rating agencies cited certain key drivers for South Africa’s downgrades. Weak growth in South Africa’s GDP was considered by Fitch, Moody’s and Standard & Poor’s as a common driver in the downgrades. Sizeable contingent liabilities and deteriorating governance were also cited as drivers of the downgrades. According to Moody’s, the weakening of South Africa’s institutional framework cast doubt over the strength and sustainability of the recovery in growth and the stabilisation of the debt-to-GDP ratio over the near term.

The leading credit agencies have devised separate criteria to rate debt that is repayable from cash flows arising out of the ownership and operation of projects or facilities. The ratings are used to assess the creditworthiness of project finance agreements.

Fitch’s ratings include an assessment of the following factors:

- Completion risk, including delay risk, cost structure, technology risk and liquidity support or credit enhancement

- Operation and revenue risk, including operating cost, demand, revenue and infrastructure renewal risk

- Debt structure, including priorities, amortisation, maturity, interest risk and hedging, liquidity, reserves, financial covenants and creditors’ rights

- Financial flexibility, including counterparty (off-taker, concession grantors and warranty providers) risk and

- Macro risks, including country risks, industry-specific risks and mitigating factors

Generally, sub-investment-grade ratings are associated with higher risk, which may result in higher borrowing costs for the rating holder. The presence of the perceived risk related to governance (such as regulatory, fiscal, political and macroeconomic risk) is relevant particularly to foreign investors, since a country’s ability to service its foreign debt or equity depends on capital mobility and currency convertibility policies, regardless of whether a project is bankable. The perception of credit rating agencies may be influential to a foreign investor’s assessment of risk in this regard. If, for example, as a result of a weaker institutional framework assessed by credit rating agencies, the measures that the South African government will take in situations of financial distress (such as direct intervention to control foreign exchange markets) are uncertain, investors may require assurance that a foreign currency loan obligation is capable of being serviced in a timely manner. Accordingly, if foreign investors perceive a higher sovereign risk in South Africa following the downgrades, they may demand a higher premium to invest in a project.

The “Basel III: A Global Regulatory Framework for More Resilient Banks and Banking Systems” report published by the Basel Committee on Banking Supervision requires an increase in the quantity of capital to be held by banks, making non-recourse lending difficult. In particular, Basel III requires banks to keep funding in place of at least one year in maturity for their long-term asset bases of one year maturity or more. While the term of the capital to be maintained need not cover the full term of the asset and Basel III continues to allow banks to be indebted for shorter terms than its loans, the lengthy maturity periods of project loans may require banks to secure funding for periods longer than one year. The additional funding required to be held by banks under Basel III for purposes of a long-term investment in a country with increased sovereign risk may further erode appetite in the banking sector to fund projects.

Sub-investment-grade ratings are also problematic to institutional investors. Asset fund managers are required to comply with the provisions set out in Regulation 28 under the South African Pension Funds Act, 1956. Among others, Regulation 28 prescribes asset limits, requires asset managers to maintain an investment policy and stipulates certain investment principles to be followed by asset fund managers. In terms of these principles, an asset fund manager may take credit ratings into account, but it may not rely on them to assess risk. Such principles further require asset fund managers to perform due diligence on investment opportunities to account for credit, market and liquidity risks as well as operational risk for assets not listed on a stock exchange. Due to the requirements of Regulation 28, asset fund managers often implement a policy that restricts investments to investment-grade assets.

Credit ratings comparisons on the continent

Compared to its BRICS peers, South Africa is ranked similarly to Russia and is a notch above Brazil, while India maintains a lower medium-grade rating and China boasts upper medium and high-grade ratings. Moody’s anticipates a negative outlook for the creditworthiness of sovereigns in sub-Saharan Africa for 2017, driven mainly by the liquidity stress facing commodity-dependent countries including recurring fiscal deficits, subdued economic growth and persistent political risk. By the end of 2016, Moody’s downgraded seven sovereigns in sub-Saharan Africa by an average of around two notches, with a total of 29 of the 134 countries rated by Moody’s downgraded globally.

With the exception of Botswana, which holds upper medium-grade ratings from Standard & Poor’s and Moody’s (A- and A2 respectively), South Africa’s credit ratings collectively rank above the rest of sub-Saharan Africa, the majority of which hold highly speculative ratings. The only other higher-rated sub-Saharan African countries in 2017 are Mauritius and Namibia. Nevertheless, according to Moody’s, South Africa’s institutions are, on average, stronger than those in other emerging markets.

Assertive infrastructure investment is required across the continent in order to address infrastructure deficits and create future growth. However, where the presence of sovereign risk is recognised, credit rating agencies may cap the rating of project finance transactions in emerging economies at the level of the relevant sovereign’s rating. According to a recent policy brief by the Brookings Institution, the three main external sources of infrastructure finance in Africa are: a) official development finance (primarily from the World Bank and the African Development Bank); b) participation by the private sector (primarily in telecommunications, transport and energy projects); and c) official Chinese financing (primarily in the transport sector), which collectively account for 97 per cent of all such external investments.

Figure 1: Moody’s credit ratings

Figure 2: Fitch’s credit ratings

Figure 3: Standard & Poor’s credit ratings

Figure 4: Major credit ratings agencies: Ratings scales and definitions

{kind=link}

Source: Fitch Ratings, Definitions of Ratings and Other Forms of Opinion, August 2012. Moody’s Investors Service, Ratings Symbols and Definitions, June 2012. Standard & Poor’s, Standard and Poor’s Rating Definitions, June 2012.

Options for enhancing project credit risk

The outlook of credit rating agencies is not all pessimistic. Agencies have identified the following credit strengths maintained by South Africa:

- Deep domestic financial markets

- A sound banking sector, which has a Fitch Bank Systemic Risk Indicator of ‘BBB’

- A well-developed macroeconomic framework

- Low foreign currency debt

- Continued adherence by South Africa’s institutions to its Constitution, accountability and the rule of law

- A favourable government debt structure and

- A track record of fairly prudent fiscal and monetary policy

While sovereign guarantees are useful to protect investors, Moody’s has identified as challenges to South Africa’s creditworthiness the emergence of liquidity pressures on state-owned companies that require government intervention, such as the provision of guarantees. Accordingly, the cost of financing associated by perceived sovereign risk may be tempered by the availability of third-party guarantees, particularly those provided by institutions holding a higher credit rating than the government, and other contractual security arrangements, such as collateral or insurance. Historically, the support of official agencies has been essential to projects in African countries. Development finance institutions (such as the Overseas Private Investment Corporation and the Multilateral Investment Guarantee Agency) as well as public and private export credit agencies (such as the Export-Import Bank) have also in the past reliably mitigated risk to investors through loan guarantees, political risk insurance and subordinated equity. Monoline insurance companies such as MBIA and AMBAC may be engaged to provide insurance coverage for development and construction risk.

As an alternative to a sovereign guarantee, a put/call option was applied in a power project in Nigeria in terms of which the government agreed to purchase the power plant at a certain price in the event that the off-taker defaulted. As this model would have no effect on a country’s balance sheet, it would not affect a country’s credit rating.

Banks may require non-bank investors, including pension funds, private equity funds and other asset funds, to supplement the funding of projects. Pension funds have recently emerged as investors in projects. The South African Government Employees’ Pension Fund has invested in solar power and telecommunications projects. The tendency of pension funds to invest in fixed-income bonds makes them suitable investors in long-term, capital-intensive projects. Regional infrastructure funds, such as the Pan-African Infrastructure Development Fund, the Africa Development Bank’s Africa50 Fund and the COMESA Infrastructure Fund, may also prove to be a useful source of project finance in the future.

The bond market is currently a topical source of funding for projects. The liquidity of project bonds and their other regulatory advantages allow them to meet demands that banks cannot. In order to facilitate the use of project bonds in South Africa, the JSE Limited is currently developing a new listing framework for project bonds.

Further, high-rated bonds require less funding than similarly rated loans under the proposed net stable funding ratio requirement in terms of Basel III.

An even more attractive option is for bonds to be issued directly by highly rated institutions such as multilateral banks to fund projects and repaid by the government through a loan by the institution.

Prospects for South Africa

It is noteworthy that the World Bank recently announced its plan to provide US$57 billion in financing for sub-Saharan African countries over the next three fiscal years, a portion of which is expected to be allocated to infrastructure projects such as access to water and power.

Overall, the strengths identified by credit rating agencies indicate a well-established independent judiciary and impartial regulatory systems that allow access to a variety of financing products and platforms. Unlike in other African countries, it is expected that project finance in South Africa will continue to involve a mix of investors, which reduces the risk to a particular partner. This, together with the perceived profitability of project finance transactions, may be sufficient to override certain sovereign risk concerns.

As project bonds are generally rated in terms of methodologies that are distinct from those used to rate the country hosting the project, it may prove to be easier for credit rating agencies to rank project bonds higher on the rating scale than a host country, particularly where credit enhancing measures are applied. For example, a recent bond issued by the City of Johannesburg was rated ‘AA-‘ by Fitch due to the partial credit guarantees for up to 40 per cent of the principal amount provided by International Finance Corporation (which holds a ‘AAA’ long-term issuer credit rating from Standard & Poor’s) and the Development Bank of Southern Africa.